We round up the essential information you need to know about price displays and payments made in 2023 for goods and services to be delivered in 2024.

Price Displays – What Should I See?

GST-registered businesses must display GST-inclusive prices on their price displays to the public. What you see must be the final price you pay. From 1 January 2024, the prices displayed by GST-registered businesses must be inclusive of GST at 9%[1]. Businesses that are unable to switch their price displays overnight may display 2 prices:

- One applicable before 1 Jan 2024 showing prices inclusive of GST at 8%

- One applicable on/after 1 Jan 2024 showing prices inclusive of GST at 9%

[1] When purchasing from 24-hours stores from 12 a.m. to 7 a.m. on 1 Jan 2024, you may be charged GST at 8% on your purchase if it is the supplier’s normal accounting practice to treat the sales made during this time as sales of the preceding day.

An exemption is granted to hotels and F&B establishments[2] that impose service charge on their goods and services. They are not required to display GST-inclusive prices for goods and services that are subject to service charge to ease their operations. However, they must still display a prominent statement informing customers that the prices displayed are subject to GST and service charge.

Businesses that do not comply with price display requirements may be subject to a fine. Businesses cannot charge and collect GST at 9% before 1 Jan 2024.

[2] Excluding hotels and F&B establishments that do not impose a service charge, and F&B establishments that levy a nominal service charge without genuine business reasons other than to avoid displaying GST-inclusive prices.

Payments – What Is the Correct GST to Pay?

For transactions that span 1 Jan 2024, GST transitional rules may apply. A transaction is considered to span the GST rate change if one or two of the following events takes place wholly or partially on/after 1 Jan 2024:

- The issuance of invoice by supplier

- The receipt of payment by supplier

- The delivery of goods or performance of services

Here are some scenarios that you might find yourself in.

The supplier delivers the fridge to me on 3 Jan 2024.

A. I make full payment for the fridge on 3 Jan 2024 after receiving the item.

The supplier is required to charge 9% on payment made on/after 1 Jan 2024 even though the invoice received on 29 Dec 2023 would reflect GST at 8%. The supplier may collect the additional 1% GST from you such as by issuing an additional invoice. However, if the supplier chooses to absorb the additional 1% GST, no additional GST will be collected from you.

B. I make full payment for the fridge on 30 Dec 2023 before receiving the item.

GST is charged at 8% on payment made in 2023 even though the goods are delivered on/after 1 Jan 2024.

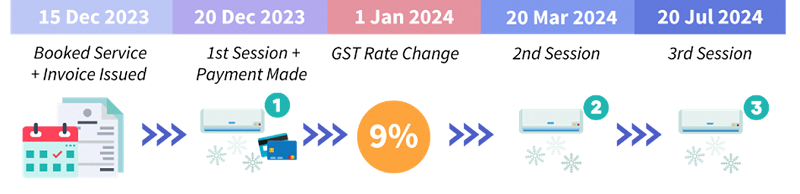

I receive the invoice for all sessions on the same day. The aircon servicing will be performed on 20 Dec 2023, 20 Mar 2024 and 20 Jul 2024.

A. I make full payment for the 3 sessions on 15 Jan 2024.

The supplier may collect the additional 1% GST of $5 ($500 x 1%) from you such as by issuing an additional invoice. However, if the supplier chooses to absorb the additional 1% GST, no additional GST will be collected from you.

B. I make full payment for the 3 sessions on 20 Dec 2023.

GST is charged at 8% on payment made in 2023 even though the services are performed on/after 1 Jan 2024. You will pay $810 (i.e. $750 plus 8% GST of $60) to the supplier.

I pay the deposit of $200 (excluding GST) on 18 Nov 2023 to confirm the booking and receive a receipt from the supplier. The supplier will issue the invoice and I will make payment for the remaining amount of $800 (excluding GST) after the dinner on 10 Feb 2024.

GST is charged at 8% on payment made in 2023 and at 9% on payment made after 1 Jan 2024. In this case, GST is charged at 8% on the $200 deposit paid before 1 Jan 2024 and 9% on the balance payment of $800 received on/after 1 Jan 2024.

I opt for a 10-months interest-free instalment payment plan and I make my first instalment payment in Dec 2023. The supplier delivers the vacuum cleaner to me on 3 Jan 2024.

A. The instalment payment plan is arranged with the supplier.

When the instalment plan is arranged directly with the supplier, the supplier will receive the payments progressively. GST is charged at 8% on payments made in 2023 and 9% on payments made on/after 1 Jan 2024. Hence, you will pay 8% GST on the first instalment payment of $100 paid in 2023 and 9% on the subsequent instalments paid on/after 1 Jan 2024.

B. The instalment payment plan is arranged with the bank via credit card payments.

When the instalment plan is arranged with the bank via credit card payments, the supplier will receive the full payment from the bank upfront once payment is charged to your credit card. Therefore, where the full payment is charged to your credit card by 31 Dec 2023, you will pay 8% GST on the full amount. This is the case even though you may be making the credit card instalment payments to the bank only in 2024.

I also received an invoice on 10 Dec 2023. On 26 Dec 2023, I decide to change to another training course, which is scheduled to take place on 20 Jan 2024. The new training course is valued at $1,200 (excluding GST). I make payment for the difference on 2 Jan 2024.

A. The service provider does not refund the payment to me but directly sets off the payment previously made against the fees for the new course.

Part payment for the new training course is considered as made in 2023 as the supplier directly sets off the payment of $1,000 previously made against the new course fees. Hence, GST remains at 8% on the payment of $1000 (excluding GST) made on 10 Dec 2023. However, you will pay GST at 9% on the additional fee of $200 for the new training course.

B. The full payment of $1,000 is credited to my account with the service provider. I use the credit to pay for the new training course in Jan 2024.

GST is chargeable at 9% on the full course fee of $1,200 since the credit is only utilised on/after 1 Jan 2024 to pay for the new training course.

The jacket costs less than $400 while the handbag costs over $400. I make payment upon checkout on 23 Dec 2023. The items are separately imported by air into Singapore on 5 Jan 2024.

Purchase of jacket

Since 1 Jan 2023, GST is chargeable on sales of low-value goods by GST-registered overseas sellers. Low-value goods are goods with sales value at/below S$400 and which will be imported via air or post after the sale. GST is charged at 8% on low-value goods purchased in 2023 and at 9% on low-value goods purchased on/after 1 Jan 2024. Hence, you will pay 8% GST to the overseas seller for the jacket purchased in 2023.

Purchase of handbag

The handbag is not an LVG. Hence, GST is not charged by the GST-registered overseas seller at the point of sale. However, import GST will be collected on non-LVGs at importation. 8% GST will be collected on goods imported in 2023 and 9% on goods imported on/after 1 Jan 2024. Hence, you will pay 9% GST to Singapore Customs for the handbag imported after 1 Jan 2024. To facilitate the importation of goods, the overseas seller may collect import GST at the GST rate of 9% from you in advance, for payment to Singapore Customs.

The maintenance services are valued at $300 (excluding GST) for each quarter. On 1 Nov 2023, I receive an invoice for quarterly maintenance services from Dec 2023 to Feb 2024, with payment for the invoice due by 15 Dec 2023. On 15 Dec 2023, I make a payment of $1,296 to the MA for 1-year of maintenance services from Dec 2023 to Nov 2024 even though the MA has yet to issue invoices for the period after Feb 2024. The MA does not refund the excess payment and treats the excess payment as a credit balance in my account to offset my future liability for payment of maintenance fees.

- 8% on maintenance fees for the period from Dec 2023 to Feb 2024. This means that you will pay $324 (i.e. $300 plus 8% GST of $24).

- 9% on the maintenance fees for the period from Mar 2024 to Nov 2024. This means that you will need to pay $981 (i.e. $900 plus 9% GST of $81). You will be required to top up $9 for the additional 1% GST.

RELATED ARTICLES